DoubleDown Interactive: The Stock That Trades Above Its Buyout

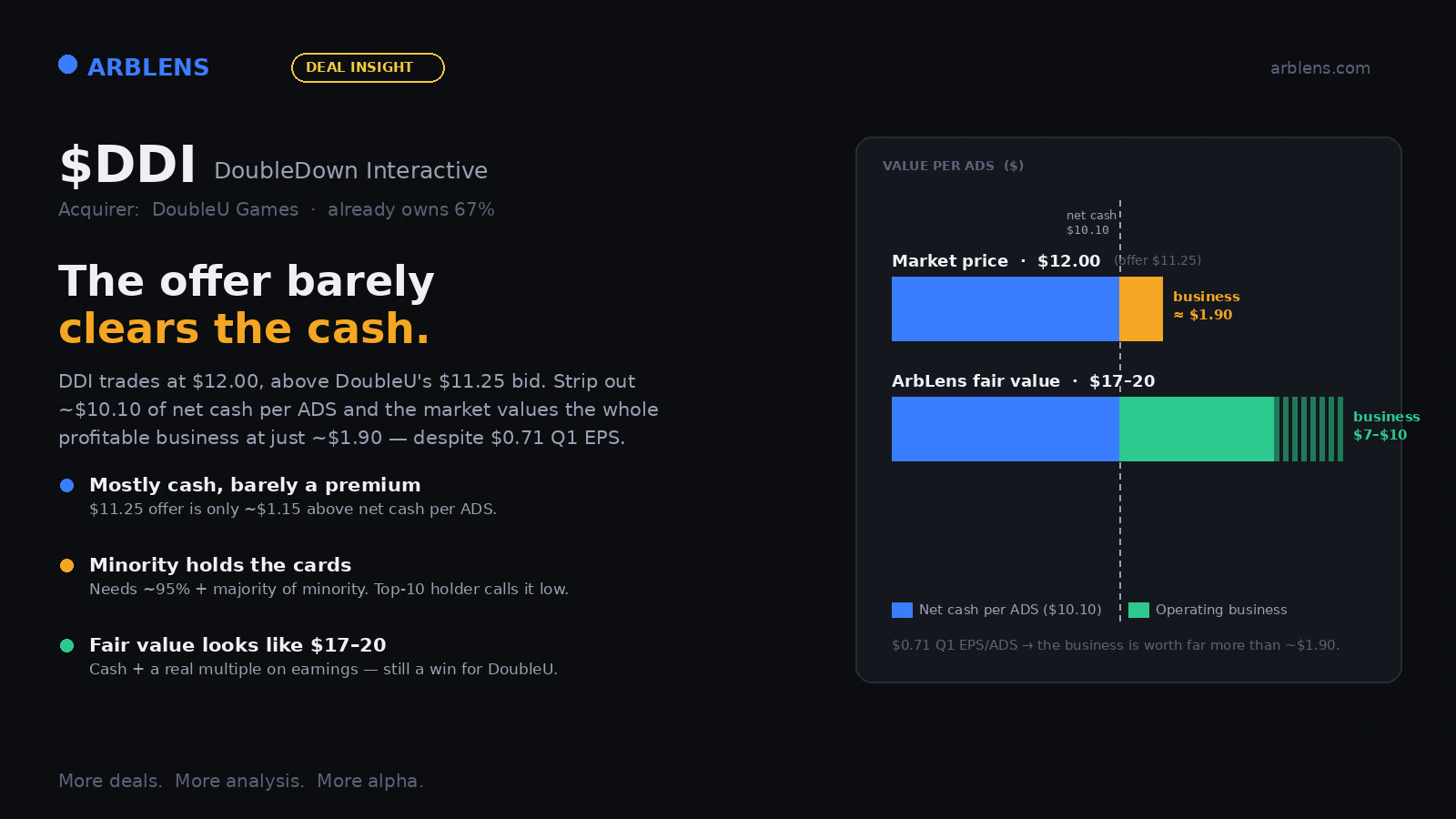

DoubleDown Interactive ($DDI) is a cash-rich, highly profitable social-casino company. Its Korean parent — already a ~67% owner — has offered to take it private at $11.25 per ADS. The stock trades above that offer. Strip out ~$10.10 of net cash per ADS, and the market is valuing the entire profitable business at roughly $1.90. This isn't typical merger arbitrage — it's a cash-backed special situation with a live catalyst.

The shape of the bet in one view — a small, capped downside against several multiples of potential upside (illustrative estimates from ~$12, not predictions):

| Scenario | Target | Potential move |

|---|---|---|

| Deal closes at $11.25 (no change) | $11.25 | −6% |

| DoubleU raises its bid | $17–20 | +42% to +67% |

| Deal breaks, stock re-rates to peers | $20–35 | +67% to +192% |

This is not your typical merger arbitrage. The "buyer" isn't an outsider — it's the controlling shareholder. DoubleU Games, a Korean gaming company, already owns roughly 67% of DoubleDown Interactive (NASDAQ: DDI) and has proposed buying the remaining ~33% it doesn't own at $11.25 per ADS in cash, taking the company fully private and delisting it.

Two features make this unusual. First, the stock trades above the offer (~$12.00 vs $11.25). When a target trades over the bid, the market isn't pricing the deal closing at terms — it's pricing a higher price or a broken deal. Second, the minority holds the leverage: taking a controlled company private like this needs near-unanimous share support plus a majority of the unaffiliated minority. Because DoubleU already controls two-thirds, it effectively needs the minority's consent — and at least one holder is pushing back. Four Tree Island Advisory, a top-10 shareholder, has publicly called $11.25 inadequate.

In plain terms, DDI is a digital casino-entertainment company that makes most of its money selling virtual chips in free-to-play games. It runs two segments: a dominant Social Casino business (~80–85%) — free-to-play slots, poker, table games and bingo monetized through in-app purchases — and a smaller, growing iGaming business (~15–20%) offering real-money online casino games, mainly in Europe through the SuprNation and WHOW Games brands.

The social-casino engine is the story: players don't have to spend, but enough do that the model throws off cash at gross margins frequently above 70%, with modest capital needs. The flagship DoubleDown Casino, alongside DoubleDown Classic and Fort Knox, anchors a mature, cash-generative franchise. Not a high-growth story — a genuinely profitable one.

Here's what makes this a special situation rather than just a cheap stock. Break the share price into its two parts: roughly $10.10 of net cash per ADS sits on the balance sheet, which means that at ~$12.00 the market assigns just ~$1.90 to the entire operating business.

That ~$1.90 is what the market pays for a business that earned $0.71 per ADS in Q1 alone — roughly $2.80 annualized. That's an implied multiple of well under 1x annual earnings: the market is paying less for the entire operating business than it earns in a single year. For a profitable, high-margin, cash-generative company, that is extraordinarily low. Put differently: you're not really betting on the business succeeding — you're mostly buying cash, with a profitable business attached for a couple of dollars.

The cleanest public comparable is Playtika (PLTK), the largest pure-play social-casino operator. Here's how the space tends to be valued on forward earnings:

| Company / Segment | Forward P/E | Notes |

|---|---|---|

| Playtika (PLTK) | ~6x | Closest peer; discounted for slower growth |

| Social casino / mobile gaming | 6x–12x | Depends on growth and margins |

| Broader iGaming / online gambling | 8x–15x | DraftKings, Flutter and similar names |

| DDI (current) | ~5x or lower | Distorted by the takeover overhang |

A normal range for a high-margin, cash-generative name like DDI would be roughly 8x–12x forward EPS. Even Playtika — penalized for slow growth — trades around 6x, the conservative end of the sector. DDI sits at ~5x or below, almost entirely because the takeover has frozen the multiple. Lift the overhang, and a re-rating toward peer levels is the natural pull.

The downside is cushioned by cash; the upside is leveraged to a re-rating or a higher bid. The scenarios below are illustrative estimates, not predictions — but they frame the shape of the bet, where the realistic downside is small and several upside paths are multiples of it.

🟢 Path 1 — A Higher Bid ($17–20)

The approval structure forces DoubleU to negotiate. A bump into the $17–20 range (+42% to +67%) would still be a bargain for DoubleU — it's buying a cash-rich, profitable business — while giving the minority fair value for the cash plus the earnings.

🟢 Path 2 — The Deal Breaks & Re-Rates ($20–35)

If the committee rejects $11.25 and DoubleU walks, the overhang lifts and the market can re-focus on fundamentals — cash plus a real multiple on earnings. A re-rating toward peers points to $20–35. This is the bull scenario and isn't automatic (see the risks below).

🔴 The Downside — Deal Closes As-Is ($11.25)

If the minority's leverage fails and the deal simply closes at $11.25, you're capped at roughly −6% from today. Even a clean break is cushioned by the ~$10 net-cash floor. The realistic downside is small — that's the entire point of the setup.

Most setups depend on a single outcome. This one has two independent paths: the deal succeeds at a higher price, or the deal breaks and the stock re-rates to fundamentals. You don't need to predict which. You need the "$11.25 with no improvement" outcome to be the least likely one — and the minority's leverage plus the public pushback argue that it is.

The special committee of independent directors is still reviewing the offer. Four Tree Island Advisory (top-10 holder) has publicly argued the bid is too low. That creates pressure for either a higher bid or a rejection — a roughly binary outcome likely to resolve over the coming weeks or months. Event-driven, with a defined decision point, is exactly the profile special-situations investors look for.

No setup is free money. The honest bear case:

What Can Go Wrong

The deal closes at $11.25 anyway. The minority's leverage isn't absolute; if enough holders tender or the committee blesses the price, you're capped at a small loss and the upside evaporates.

"Deal breaks" doesn't guarantee a pop. DDI traded near $9.19 before the offer. A clean break could drift toward the ~$10 cash floor rather than re-rate to $20–35, at least initially — the re-rating depends on the market choosing to reward fundamentals.

Controlled-company dynamics cut both ways. DoubleU is a patient parent, not a motivated outside buyer on a financing clock. It can walk, wait, and re-approach on its own timeline. The minority can win a battle and still be stuck in a controlled, illiquid stock.

Dead money / time risk. Even a good outcome can take time; capital parked here earns nothing while you wait.

Liquidity & regulation. DDI is a thinly traded ADS with a ~33% public float, and the European iGaming segment carries licensing risk the social-casino segment does not.

The cash backing is why the downside is cushioned — but cushioned is not guaranteed. Treat the floor as strong support, not a contractual put.

DDI is a rare combination: a profitable, cash-rich business the market values at almost nothing, wrapped in a controlled-company take-under where the minority holds unusual leverage, with a live, near-term catalyst. The downside is anchored by ~$10.10 of net cash per ADS; the upside runs through either a higher bid or a post-break re-rating.

It won't suit everyone — controlled-company situations can be slow, illiquid, and frustrating, and a break could mean dead money before it means a re-rating. Know which bet you're making. But on the numbers, the reward looks like a multiple of the risk — and the situation is depressed for a reason that has little to do with the quality of the underlying business.

Track DDI and 50+ active deals with live spreads, spread history charts, and deal analysis.

View Live Tracker →Get merger arb insights and special situations delivered to your inbox.