Tiptree: The 40% NAV Discount

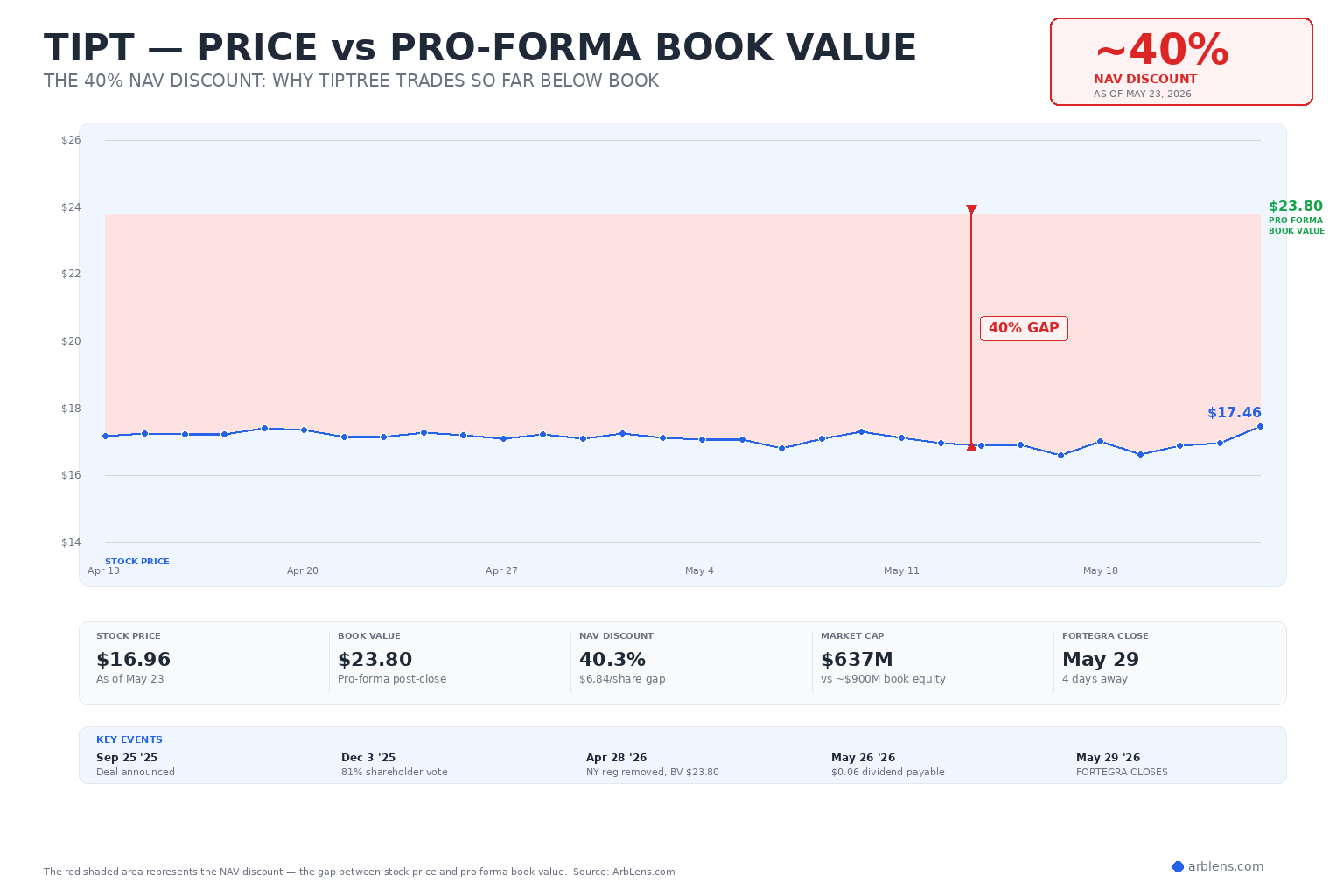

Tiptree is selling its crown jewel — specialty insurer Fortegra — for $1.65 billion in cash. The deal closes Thursday. After closing, Tiptree's pro-forma book value is $23.80 per share. The stock trades at $16.96. That's a 40% discount to the cash that's about to be sitting on the balance sheet. This is not merger arbitrage. This is a governance bet.

In September 2025, Tiptree agreed to sell Fortegra — a Jacksonville-based specialty insurer focused on warranty, credit, and niche P&C products — to South Korea's DB Insurance for $1.65 billion in cash. It was the largest US market entry by a Korean non-life insurer. Shareholders approved 81% in December 2025. The merger agreement was amended April 28 to remove a New York regulatory condition, clearing the final hurdle.

The deal closes May 29. That's four days from today. This is not in dispute. The question isn't whether Fortegra gets sold — it's what happens to Tiptree after.

Post-close, Tiptree becomes a cash-rich holding company. The Fortegra proceeds, minus debt paydown, taxes, transaction costs, and the Warburg Pincus minority buyout, leave Tiptree with an estimated $23.80 per share in pro-forma book value. The stock trades at $16.96. The gap is $6.84 per share — roughly 40%.

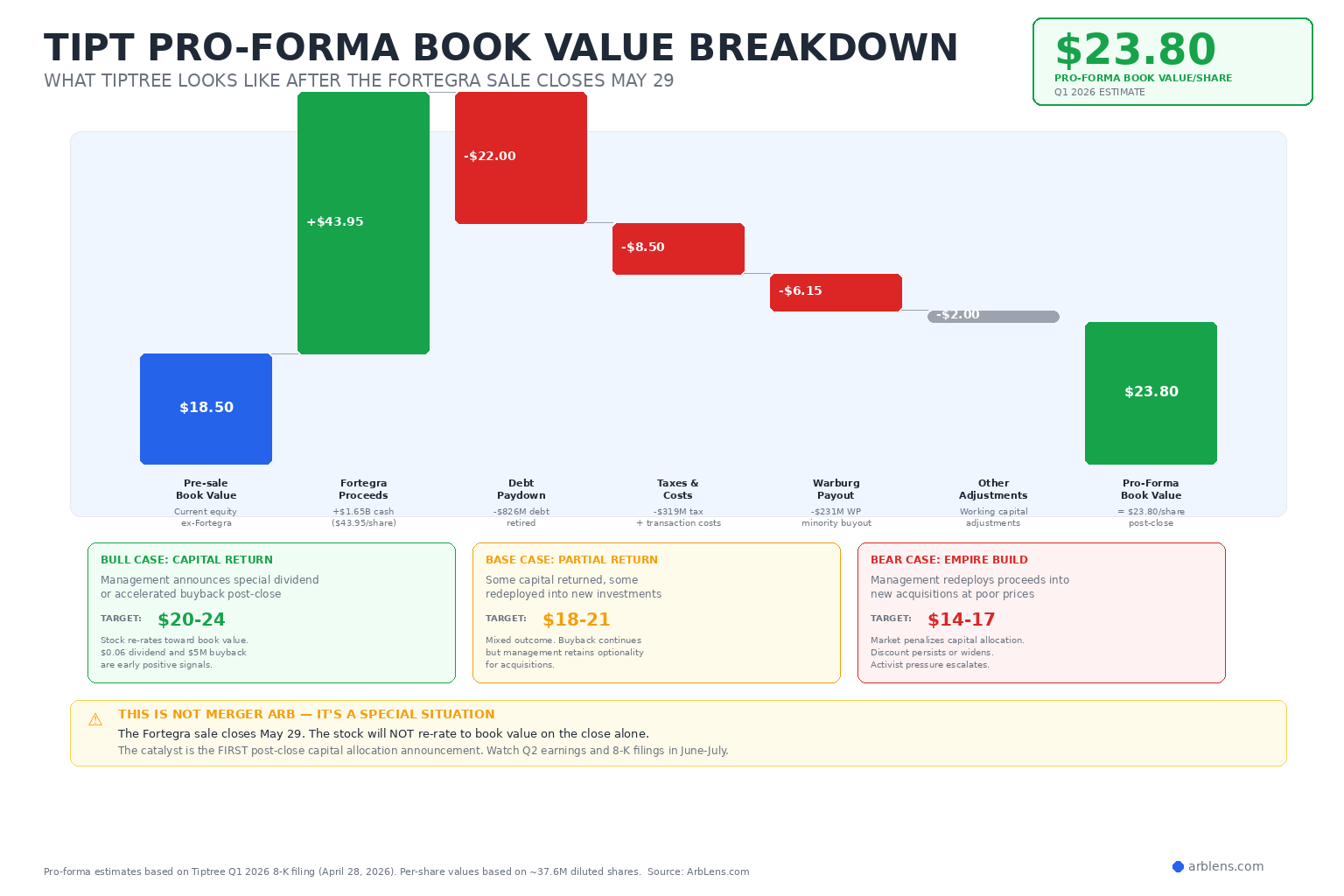

Tiptree disclosed the revised pro-forma book value of $23.80/share in its Q1 2026 8-K filing on April 28 (down from an earlier $24.40 estimate). Here's how the math works:

The starting point is Tiptree's equity excluding Fortegra (~$18.50/share). Add the full $1.65B Fortegra sale proceeds ($43.95/share). Then subtract: debt retirement (~$22/share), taxes and transaction costs (~$8.50/share), the Warburg Pincus minority payout (~$6.15/share), and working capital adjustments (~$2/share). What remains is $23.80 per diluted share in pro-forma book value.

The key number investors focus on is the net cash per share after all obligations. Not all of the $23.80 is liquid cash — some is tied up in Tiptree's remaining smaller businesses (Reliance First Capital, other investments). But the majority is cash or near-cash. The market is applying a 40% discount to this figure.

This is the central question. If Tiptree is about to have ~$900M in cash against a $637M market cap, why doesn't the stock trade at book value?

Reason #1: Management Trust Deficit

The market doesn't trust Tiptree's management to return the cash. Activist investor Veradace Partners (5% holder) has publicly argued that management historically transferred more than 5% of company value to themselves annually through compensation, related-party transactions, and fees. If management redeploys the Fortegra proceeds into new acquisitions rather than returning capital to shareholders, the discount persists or widens. The $5M in Q1 buybacks and $0.06/share dividend are positive signals but far too small to close a $6.84/share gap.

Reason #2: Post-Fortegra Uncertainty

Without Fortegra, what is Tiptree? It's a holding company with a collection of smaller, less profitable businesses and a lot of cash. The market doesn't know what comes next — special dividend? Aggressive M&A? Slow wind-down? The company has given no hard commitment on capital allocation post-close. The SEC filings even include going concern language (likely boilerplate, but not reassuring).

Reason #3: Micro-Cap Neglect

Tiptree has a $637M market cap and one analyst covering it. It trades with low volume and wide bid-ask spreads. Institutional investors who might normally arb this discount can't build meaningful positions without moving the stock. The inefficiency persists because nobody with enough capital is paying attention.

🟢 Bull Case: Capital Return ($20-24 target)

Management announces a significant special dividend or accelerated buyback program within 60 days of closing. The $5M Q1 buyback and $0.06 dividend are early signals of intent. Activist pressure from Veradace intensifies. Stock re-rates toward book value as the discount narrows. If Tiptree returns $8-10/share in cash, the stock reprices to $20+ quickly. This is the highest-probability positive outcome — management knows the market is watching.

🟡 Base Case: Partial Return ($18-21 target)

Management returns some capital (moderate buyback, ongoing quarterly dividend increases) but retains significant optionality for future acquisitions. Tiptree remains a holding company actively seeking deals. The discount narrows from 40% to 15-25% as some cash comes back but uncertainty persists. This is the most likely outcome — it threads the needle between shareholder pressure and management's empire-building instincts.

🔴 Bear Case: Empire Build ($14-17 target)

Management redeploys the majority of Fortegra proceeds into new acquisitions at inflated prices. The market punishes the capital allocation, and the discount widens beyond 40%. Veradace escalates to a proxy fight but lacks the voting power to force change. The stock stays stuck or drops as the holding company discount becomes a permanent feature. This is the scenario the current price already partially reflects.

May 29 (Thursday): Fortegra sale closes. This is the mechanical catalyst, but the stock will not re-rate to book value on the close alone. The market already knows it's closing.

June-July: The first post-close 8-K filings and Q2 2026 earnings call. This is when management reveals its hand. Any announcement of a special dividend, a large buyback authorization, or a strategic review is the real catalyst. Silence or a new acquisition announcement would be bearish.

Veradace Partners: Watch for any 13D amendments or public letters. If the activist increases its stake or launches a proxy campaign, it adds pressure for capital returns.

Tiptree at $16.96 is one of the most interesting special situations in the market right now. The Fortegra sale closes this week, creating a cash-rich holding company trading at a 40% discount to book. The gap is real, the cash is real, and the catalyst timeline is short.

But this is not merger arbitrage. There is no offer price that the stock converges to on a fixed date. There is no termination fee protecting you. The upside depends entirely on management doing the right thing with the capital — and the market's 40% discount is telling you it's not confident they will.

If you believe activist pressure and rational self-interest will force a meaningful capital return, buying at $16.96 for a $23.80 book value is one of the most asymmetric setups available. If you believe management will empire-build, the current discount is a feature, not a bug. Know which bet you're making.

Track TIPT and 50+ active deals with live spreads, spread history charts, and deal analysis.

View Live Tracker →Get merger arb insights and special situations delivered to your inbox.